Germany finds itself in a predicament seeing its relations with US, Russia and China being seriously tested, risking Europe’s stability

Chancellor Olaf Scholz a few days after the Russian invasion in 2022 declared in his landmark speech that this new reality has marked a historic turning point (Zeitenwende) for his country. Indeed, the War in Ukraine shattered Germany’s postwar certainties, ending decades of reliance on cheap Russian energy, deepening entanglement with China. Now exactly 4 years later another war this time in Iran and Middle East is testing Germany’s strategic transatlantic alliance with the United States which dates back 80+ years ago with the end of World War II.

What began as a foreign-policy Zeitenwende has become an existential economic and strategic trilemma. Berlin finds itself steering between three clashing rocks (Symplegades* according to Odyssey) —its former strategic energy partner in Moscow, its largest export market in Beijing, and its indispensable security guarantor in Washington since 1945. These “triple Symplegades” have forced a painful reinvention, one that is turning industrial decline into a defense boom even as growth stagnates and old partnerships fray.

1. Russia: The Shattered Energy Partnership

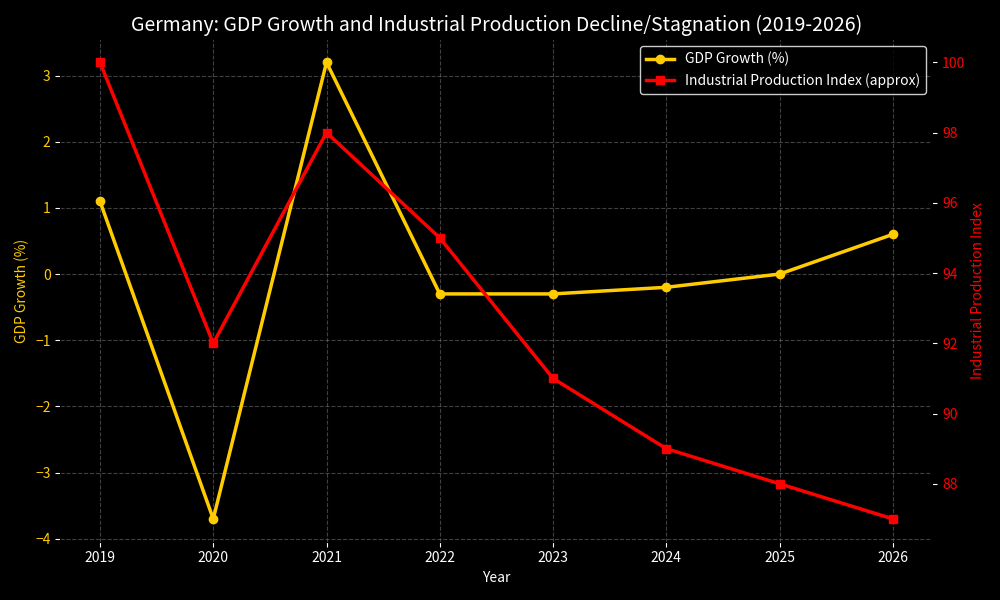

The first reality check came from Russia. For years, Germany’s economic model rested on Russian gas and oil, delivered in large part through the (Nord Stream1 & 2, Yamal Europe pipelines) and via the Brotherhood pipeline system (emphasis added!), which supplied roughly half of its natural gas needs and 20-25% of its oil. This cheap energy powered its energy-intensive export engine—automobiles, chemicals, and steel. When Russia invaded Ukraine in 2022, the resulting cutoff and sabotage of the Nord Stream infrastructure triggered an immediate energy shock: prices quadrupled, inflation surged, and industry faced existential cost pressures. Berlin responded with remarkable speed—building LNG terminals in record time, filling storages, reactivating coal plants temporarily, and accelerating the Energiewende.

Yet the scars remain. Energy costs are still 40-50% above pre-war levels, energy-intensive giants like BASF have slashed jobs and capacity, and the economy has endured its longest postwar stagnation. The war shaved roughly 1.5 percentage points off annual GDP growth, creating a structural break that lingers into 2026. Diversification succeeded in averting blackouts, but at the price of higher costs, deindustrialization fears, and a permanent break with the old “Wandel durch Handel” illusion—the long-standing belief that deep economic ties and trade with authoritarian regimes would gradually moderate them and bring political change through commerce.

2. China: The Eroding Export Lifeline

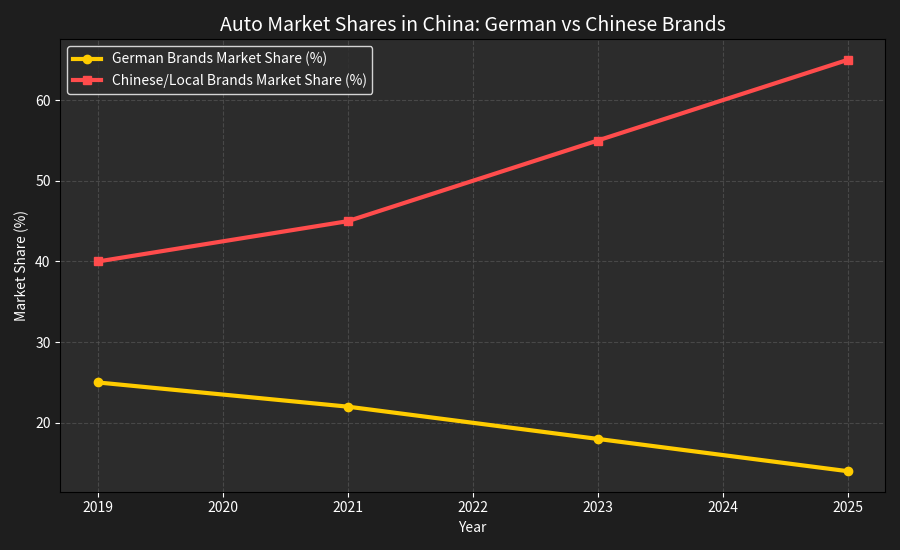

The second rock is China. Once celebrated as Germany’s growth engine and biggest trading partner (bilateral trade exceeding €250 billion annually), Beijing has become a source of fierce competition and strategic vulnerability. German carmakers—VW, BMW, Mercedes—have watched sales in China collapse: exports down roughly two-thirds since 2022, cumulative declines of 25% from 2019 peaks. Chinese EV makers like BYD dominate the local market (NEV penetration near 50%) and are now flooding Europe with cheaper, tech-forward vehicles. Machinery and chemical exports have also weakened amid Chinese overcapacity and subsidies. Berlin’s 2023 China Strategy and its 2025 update under Chancellor Friedrich Merz formalize “de-risking”: tighter FDI screening, export controls, and diversification toward India, Vietnam, and the Americas. Yet the pain is real—Germany’s trade deficit with China has ballooned, and firms face a Hobson’s choice between localizing in China or losing market share. Competitiveness has eroded; German industry, once the envy of Europe, now struggles against state-driven rivals.

3. The United States: Iran War fractured the Transatlantic Anchor

The third and most recent peril is the United States—the strategic partner that anchored West Germany’s security since 1945. Tensions that simmered under earlier trade disputes have erupted into open strain in spring 2026. Chancellor Merz, usually measured, stunned audiences by declaring that Iran’s leadership is “humiliating” the United States in the ongoing Middle East conflict, accusing Washington of entering the war without a convincing strategy or exit plan. “An entire nation is being humiliated by the Iranian leadership,” he said. The Trump administration’s response was swift and pointed. Within days, the Pentagon announced the withdrawal of 5,000 U.S. troops from Germany over the next six to twelve months—a reduction that trims the American presence noticeably. At the same time, a Biden-era plan to deploy a long-range fires battalion equipped with Tomahawk missiles reportedly was canceled, depriving Berlin of a key deterrent against Russia. Most damaging for German industry, President Trump raised tariffs on European Union cars and trucks to 25% (from a previously negotiated lower rate), citing non-compliance with trade commitments. The move hits Germany’s auto sector—the backbone of its export economy—squarely in the gut.

From Cars to Cannons: Germany’s Industrial Pivot to Defense

Out of this triple squeeze has emerged an unexpected adaptation. As detailed in a recent Wall Street Journal article titled “Germany Is Reinventing Itself as a Weapons Factory,” Berlin is pivoting from cars to cannons, recasting industrial decline into a defense boom. With roughly 15,000 manufacturing jobs vanishing monthly—including in the once-dominant auto sector—factories, workers, and capital are being steered toward rearmament. The iconic Volkswagen plant in Wolfsburg, emblem of Germany’s postwar economic miracle, stands as a potent symbol of this transformation. As auto demand slumps under Chinese competition and now U.S. tariffs, VW and suppliers are exploring or shifting production toward military applications. Other VW facilities are in talks to produce components for systems like Israel’s Iron Dome air-defense network as early as 2027. Rheinmetall is expanding rapidly; auto suppliers are partnering on drones, ammunition, and military vehicles; third shifts are running to supply Ukraine and European allies. What was once Europe’s manufacturing engine is becoming the continent’s arsenal.

Spillover in Europe?

Yet this rapid accumulation of weapons across Europe carries profound risks, potentially marking the end of the continent’s 80-year postwar peace that has defined Germany and its neighbors since 1945. As Berlin repurposes its factories for armaments, historical fears of militarization are resurfacing among European partners wary of a resurgent German defense hegemony. These shifts intersect with contentious EU decisions on the new Multiannual Financial Framework, where leaders are pushing for a significantly expanded budget to fund defense, competitiveness, and strategic autonomy. In their joint press conference in Athens on April 25, 2026, French President Emmanuel Macron and Greek Prime Minister Kyriakos Mitsotakis advocated delaying repayment of pandemic-era Recovery Fund debt, exploring common debt instruments, and boosting EU investments to avoid falling behind the U.S. and China—while stressing that Europe’s defense build-up should complement rather than replace NATO. At the same time, frictions with France persist over the flagship Future Combat Air System (FCAS) project: disagreements between Dassault Aviation and Airbus over leadership, workshare, and timelines have pushed the €100 billion initiative to the brink, with recent ministerial talks highlighting deep industrial rivalries that threaten the entire program. For Greece, the ripple effects could prove especially painful: Germany’s subdued growth outlook is likely to reduce German tourism while dampening demand for Greek exports to its largest EU trading partner, underscoring how Berlin’s triple Symplegades reverberate across the continent and test the resilience of Europe’s fragile unity.

*DISCLAIMER: Symplegades were actually twin (not triple) mythical rocks located at the northern entrance of the Bosporus into the Black Sea. According to Greek mythology, they violently crashed together to crush ships, famously navigated by Jason and the Argonauts with the help of Athena. For the narrative purposes of the article we use figuratively triple nature in order to emphasize the challenging relations of Germany with its three strategic partners.